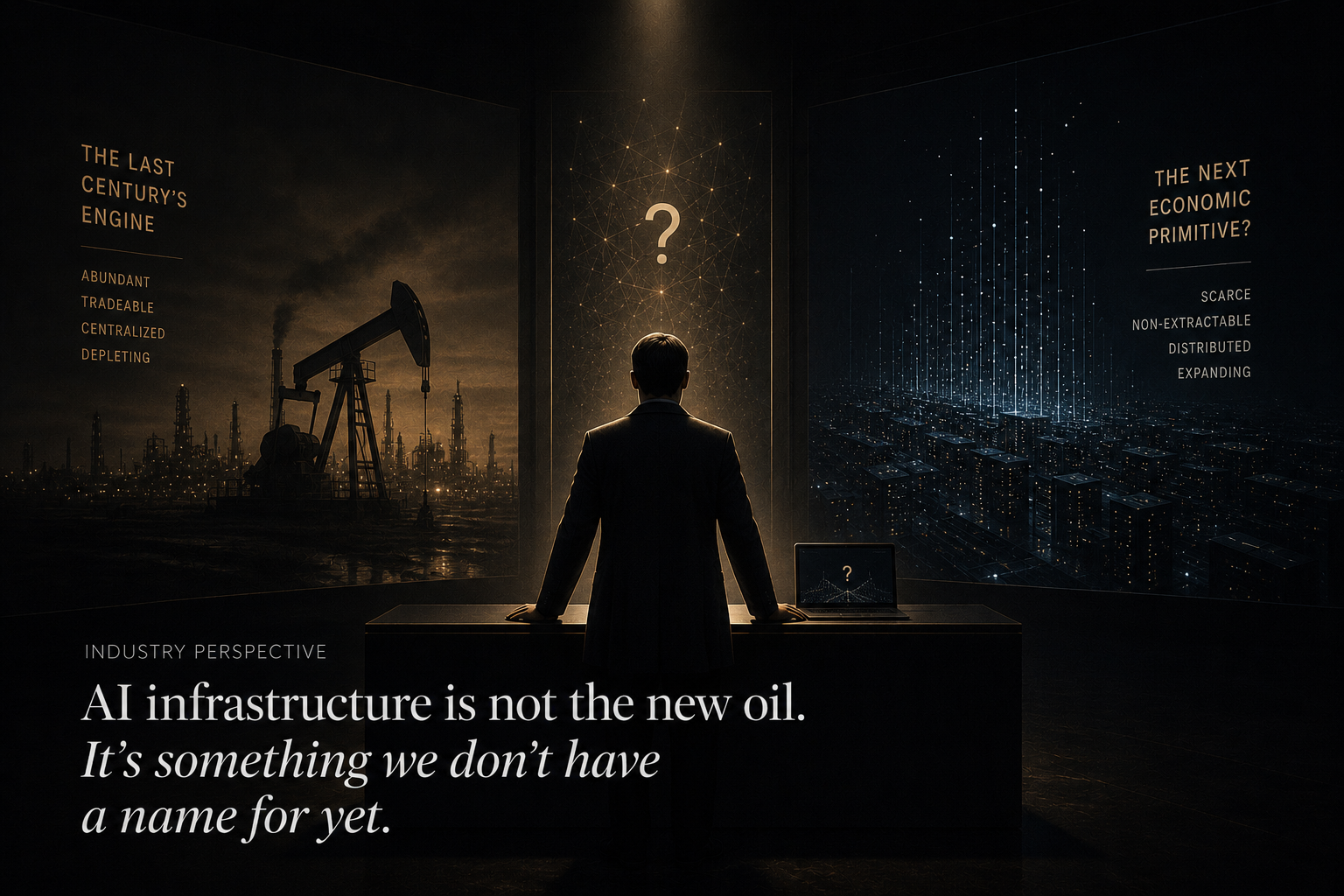

The oil analogy is seductive. I can understand why people use it. Mass fortune, tangible wealth, global strategic power, limited access players monopolizing for the rest of us, it echoes. But oil never really got to choose what you could refine.

That is the aspect of the analogy it quietly brushes aside.

The evidence for the comparison is in the numbers.

The raw data is truly staggering. In 2025, the five largest tech companies spent over $400 billion on AI infrastructure. According to McKinsey, total global data centre spending could hit $7 trillion by 2030, about the size of Japan combined with Germany in GDP. In just one year, debt issuance to finance these grew from $92 billion to $182 billion. This year alone, the four largest hyperscalers are headed to spend over $350 billion in capex.

These are oil-economy numbers. The land, power, and cooling system grab resembles a drilling boom. We discuss GPU allocations like we used to with barrel quotas. Nations are reorienting their national industrial strategy around who can build the most compute in the least amount of time.

So far, the analogy holds.

Where it breaks down

Oil is a commodity. You pump it, distill it, incinerate it. It does not have opinions on who is burning it or what they are burning it for. What a barrel of crude from Riyadh does is identical to one from Houston or anywhere. By design, the infrastructure that transfers it is neutral.

AI infrastructure is not neutral. It encodes decisions on what models get trained, with what training data and constraints, for which end customers. According to export controls once reserved for weapons and nuclear technology, the US government has classified advanced GPUs as strategic assets. Countries are now classified into tiers: 18 allies allowed to purchase anything, dozens more permitted hard limits, and around 20 nations that receive an outright ban. This is not a product supply chain policy. That large-scale thinking is a choice.

As the IEA put it bluntly in a recent report: “Countries that offer secure, affordable, fast electricity access for AI compute will be one step ahead.” But they meant first in economic output. The more worrisome knock-on effect is coming in cognitive sovereignty, or the matter of who owns building the models that operate their hospitals, their courts, their banking.

What the oil barons never had

Saudi Aramco could limit your access to fill up. It would not tell you what to do about burning it.

The hyperscalers who build this infrastructure are in a much more fundamental place. If an entire country trains its AI models on infrastructure the country does not own, tuned through APIs the country does not control, and governed by terms of service drafted by another jurisdiction, this dependence is no longer just economic. It is epistemic. It is the values and constraints of whomever built the pipes, encoded in the output, the answers, the decisions, the ranked results.

I am not suggesting malice. I am merely suggesting that the folks building this infrastructure have not fully sat with what they are building. Nor have the governments sprinting to host data centres without inquiring what runs within.

Nobody is really answering the question

$112 billion in private investment into AI made by France. India is positioning itself as a destination for compute. The Gulf states are constructing data centres like they once built refineries. Implicit in this: draw the infrastructure near and the value will flow toward you.

However, if you ran an oil economy and owned a refinery, then you owned the output. Owning the real estate while the models, weights, API keys, and governance all sit elsewhere has meant being more like a landlord who cannot read their leases in the AI economy.

These companies with the largest physical footprints are not the ones that are really creating sustainable, long-term strategic positions in this economy. They own model weights and chip architectures and training pipelines. Analyst expectations for data centre spending by the largest public developers jumped 56% in six months, according to BloombergNEF. That type of capital velocity does not have the luxury to wait for governments to work out what sovereignty even means.

The infrastructure will survive the companies that build it

This has happened before. The railroads overbilled. The fibre operators went bankrupt. The assets stayed and became the foundation for the next economy.

KKR commented directly on this trend: bubbles always damage some investors, but the space they leave behind persists. That is probably just as true here. In whatever condition the valuations happen to be in, those data centres, those power lines, and those cooling systems will find their way into something which will be around for a long time.

We do not, however, know who will govern the logic sitting on top of them. Oil had OPEC. There is nothing quite like that for Compute, and the countries that will suffer most from that absence are those who currently think only about attracting investment, without asking what must be given up with it.

Which is the conversation that the oil analogy keeps us from having.